Parking Lot Resurfacing Capitalize Or Expense

Budgeting Maintenance Costs In Parking Structures

How To Start A Parking Lot Business

Restaurant Parking Lots Does Yours Contribute To The Business Plan Kansas Asphalt Inc

How To Care For Parking Lots In Freeze Thaw Conditions Bluefin Roof Walls Pavement And Energy Consultant

Chapter 19 38 Off Street Parking Regulations And Design Development Code Duarte Ca Municode Library

Quick Easy And Permanent Asphalt Repair And Parking Lot Repair Is Possible Asphalt Repair Repair Parking Lot

Improvement decision tree final regulations considering the appropriate unit of property uop does the expenditure last updated 03 20 2015.

Parking lot resurfacing capitalize or expense. In an attempt to clarify matters the irs issued lengthy regulations explaining how to tell the difference between repairs and improvements. It may also extend the time of the depreciation deduction for several years. Illinois merchants trust co. Thus we would treat the parking lot sealing repair work as an expense and capitalize the re pavement work.

A capital improvement will add value to your property. Well on december 23. Deductible repairs and non deductible capital improvements. 103 106 1926 the court ex plained that repair and maintenance expenses are incurred for the purpose of keeping property in an ordinarily efficient operating condition over its probable useful life for the.

There has been much debate and controversy not to mention a number of court cases regarding whether or to what extent the amounts paid to restore or improve property are capital expenditures or deductible ordinary and necessary repair and maintenance expenses. Grade level surface parking area usually constructed of asphalt brick concrete stone or similar material. Capitalized asset versus expense posted on wednesday october 07 2015 share. Nationwide service 877 525 4462 kbkg com cop 2018 ll served llv 8202018 kbkg repair vs.

00 3 land improvements 15 years. If the repaving is a repair of an existing surface then it can be a repair. If this was an improvement then it can be treated as a capital expense and added to the cost basis and depreciated over time. Repairs and maintenance can be expenses fully in the year they are paid for.

All nonprofit organizations should have a capitalization policy in place. This policy sets a threshold above which qualifying expenditures are capitalized as fixed assets and depreciated. Kbkg expressly disclaims any liability in connection with use of this document or its contents by any third party. Although some of these activities such as resurfacing a parking lot or replacing portions of concrete in a parking facility may be capitalized for book purposes the activities may be considered otherwise deductible.

Parking facilities routinely undergo repairs. For more details on current vs. Any replacement work would generally be capitalized and depreciated over time. Unfortunately telling the difference between a repair and an improvement can be difficult.

Category includes bumper blocks curb cuts curb work striping landscape islands perimeter fences and sidewalks. If the lot was partially paved and only parts need to be replaced then you likely have sufficient basis to treat it as an expense. Capital expenses refer to the article current vs capital expenses. On the other side the entire cost of a repair and maintenance expense such as fixing broken windows can be immediately deducted on your taxes leaving more money in your pocket by increasing your after tax income.

Parking Fees Explained Livegreen

Glen Ellyn Park District Established In 1919 Glen Ellyn Illinois

Drivers At Thomas Jefferson Houses In East Harlem Hit By 353 Parking Rate Hike Thomas Jefferson Emergency Vehicles Jefferson

Https Www Co Walton Fl Us Documentcenter View 3235 Ldc Chapter 5 Design And Development Standards Bidid

High School Parking Lot Pothole Parking Lot Repair Asphalt Repair

Http Zoningpgc Pgplanning Com Wp Content Uploads 2016 05 Final Prd Pgc Mod 2 Div 27 5 05 09 16 Pdf

Securing Church Loans For Your Church Building Loan Church Church Building

How To Start A Parking Lot Business Small Business Chron Com

Ua Pts Program Update Parking Permit Rates 2019 2020

Palo Alto Looks To Launch Safe Parking Program For People Living In Cars News Palo Alto Online

Download A Free Home Inspection Checklist Template For Excel Or A Printable Home Inspection Form In Pdf Form In 2020 Inspection Checklist Home Inspection Selling House

Full Depth Reclamation For Parking Lot Paving For Construction Pros

10 Gantt Chart Templates Beautiful Professional And Free

Pin On Budget Template

What Are The Options For Parking Lot Sealcoating Aexcel

The Detailed Cost Breakdown To Building A New Parking Garage

Schedule C Excel Template Awesome Schedule C Expenses Template Along With Elegant Business In 2020 Small Business Expenses Business Expense Tracker Business Expense

Budget Status Budget Report Template Budget Report Template Should Be Chosen Well And Should Be Conducted For Get Budgeting Budget Template Report Template

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcruudquawzq E8mbyb4ke2znmciekdhtocmlfmspcbkckelszxd Usqp Cau

The Magical World Where Mcdonald S Pays 15 An Hour It S Australia Food Cost Mcdonalds Franchise Restaurants

Eat Live Make Living Well With Less 5 Ways To Make Every Dollar Count Ways To Save Money Living Well Ways To Save

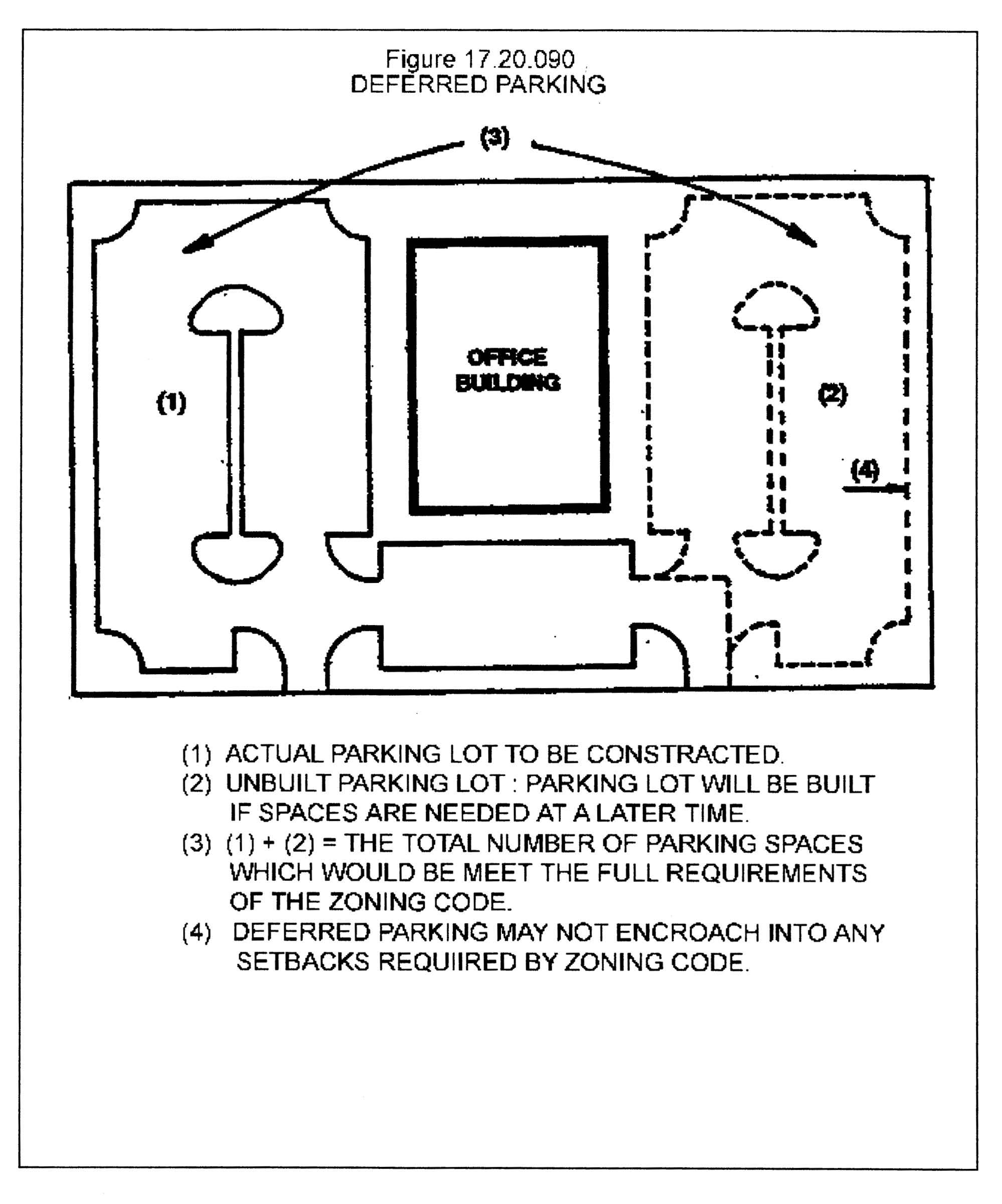

Chapter 17 20 Parking Loading And Access Code Of Ordinances Metro Government Of Nashville And Davidson County Tn Municode Library

Three Examples Of Sole Proprietorships Ehow Search Results In 2020 Balance Sheet Balance Sheet Template Sole Proprietorship

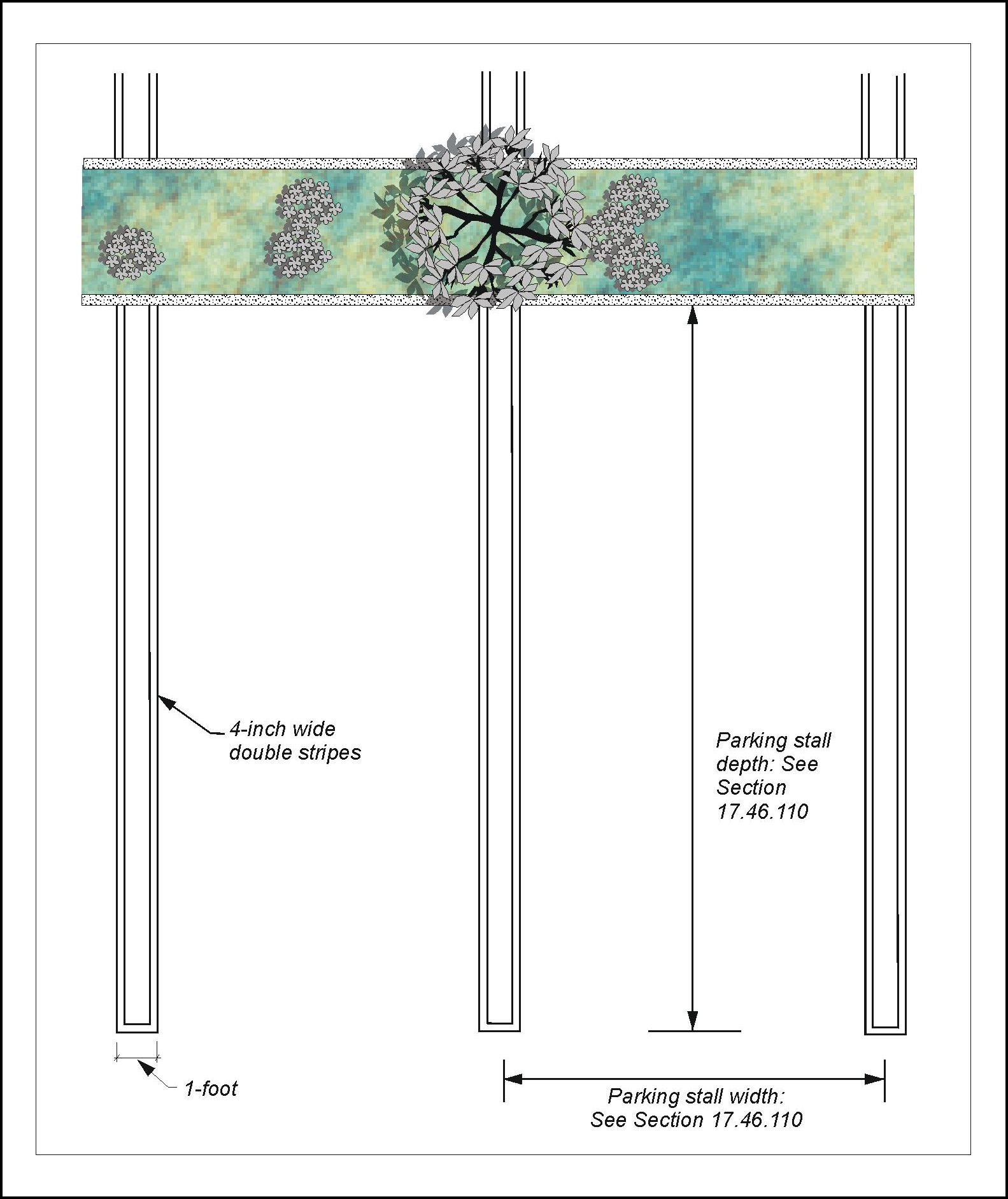

Chapter 17 46 Parking And Loading Code Of Ordinances Pasadena Ca Municode Library

متابعات الوظائف مطلوب حرفيين وعمال في مختلف المجالات للعمل بالامارات وظائف سعوديه شاغره Facilities Maintenance How To Unclog Toilet Stucco Repair

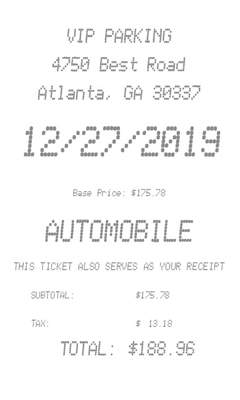

Receipts For Vehicle Parking Parking Lots Parking Garages Airport Parking

Faqs Masparc

Article 5 Supplementary Standards Uldc Pbc

Title 20 Zoning Code Of Ordinances Merced Ca Municode Library

Everything You Need To Know About The Bitcoin Halving In 2020 In 2020 Bitcoin Need To Know Marketing Data

Part 3 Parking And Loading Code Of Ordinances Orlando Fl Municode Library

15 Fun Jobs That Pay Well For Any Skill Set In 2020 Good Job Driving Instructor Finance Advice

Vehicle Maintenance Log Car Maintenance Log Fillable Etsy Vehicle Maintenance Log Car Maintenance Maintenance

Chapter 144 Zoning Code Of Ordinances New Braunfels Tx Municode Library

Https Www Vtpi Org Park Man Comp Pdf

Chapter 744 Development Standards Code Of Ordinances Indianapolis Marion County In Municode Library

Management Services For Your Business Unit For Little And Medium Sized Businesses Smbs Low Latency Solutions Provider G The Unit Management Venture Capital

9yr1ew6rrk Hvm

Http Www Bidnet Com Bneattachments 313760732 Pdf

Loading Paper Organization Organizing Paperwork Organization

Pin On Dividend Destiny

Pdf The Trouble With Minimum Parking Requirements